Warmer Summer Due to EL Nino

Syllabus: GS1/Physical Geography

In Context

- As per the IMD, India is likely to see above-normal maximum and minimum temperatures in summer due to El Nino.

About

- IMD customarily puts out a forecast for the summer season in the first week of March every year.

- The summer season is classified from March to end of May, before the monsoon season officially starts from June.

- India is likely to experience a warmer start to the summer season this year with El Nino conditions predicted to continue through the season.

- The country is likely to record above-normal rainfall in March (more than 117% of the long-period average of 29.9 mm).

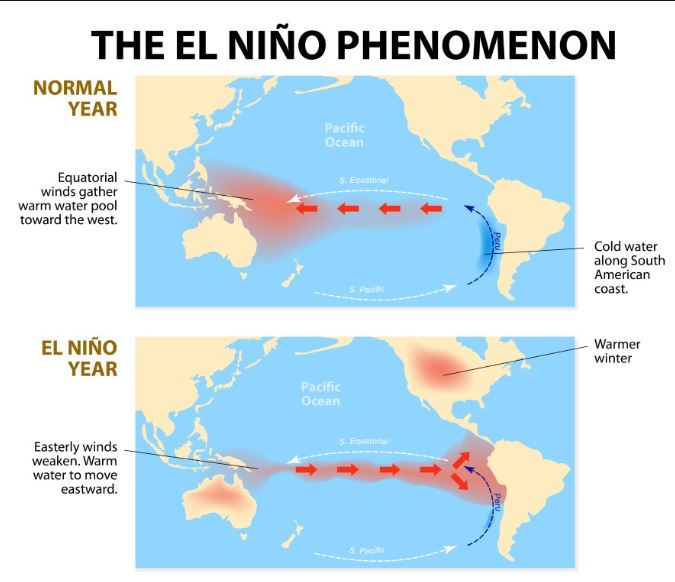

Ocean-Atmosphere system

- Normal Conditions: During normal conditions in the Pacific ocean, trade winds blow west along the equator, taking warm water from South America towards Asia.

- To replace that warm water, cold water rises from the depths — a process called upwelling.

- The warmer surface waters near Indonesia creates a region of low-pressure area, causing the air to rise upwards. This also results in formation of clouds and heavy rainfall.

- The air flow also helps in building up the monsoon system which brings rainfall over India.

- Abnormal Conditions: Both El Nino and La Nina usually begin to develop in the March to June season, reach their peak strength in the winters and then begin to dissipate in the post winter season.

- Both these phases typically last for a year, though La Nina, on an average, lasts longer than El Nino.

- While these phases alternate over a period of two to seven years, with the neutral phase thrown in between, it is possible for two consecutive episodes of El Nino or La Nina to occur.

What is El Nino?

- El Niño means Little Boy in Spanish. South American fishermen first noticed periods of unusually warm water in the Pacific Ocean in the 1600s.

- It is a climate phenomenon characterized by the periodic warming of sea surface temperatures in the central and eastern equatorial Pacific Ocean.

- During El Niño, trade winds weaken. Warm water is pushed back east, toward the west coast of the Americas and as a result cold water is pushed towards Asia.

Impact of El Nino

- Low Rainfall: El Niño often correlates with below-average monsoon rainfall in India, leading to droughts in many parts of the country. This can have severe consequences for agriculture, water resources, and the economy.

- Increased Temperature: El Niño can also lead to an increase in temperatures across various parts of India.

- Forest Fires: The drier conditions associated with El Niño can increase the risk of forest fires, particularly in regions with dense vegetation. These fires can cause environmental damage, loss of biodiversity, and air pollution.

- Water Scarcity: Decreased rainfall during El Niño events can lead to water scarcity in many parts of India. This can affect drinking water supplies, irrigation for agriculture, and hydropower generation.

- Impact on Fisheries: El Niño can also affect marine ecosystems and fisheries along India’s coastline. Changes in sea surface temperatures and ocean currents can disrupt fish migration patterns and lead to fluctuations in fish populations.

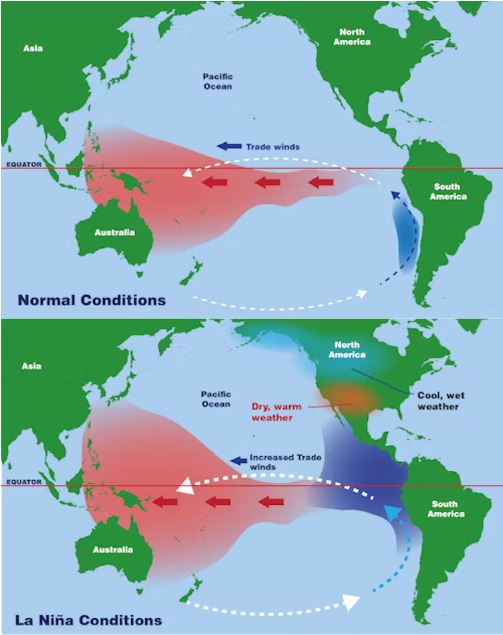

La Niña:

- It means Little Girl in Spanish. La Niña is also sometimes called El Viejo, anti-El Niño, or simply “a cold event.” La Niña has the opposite effect of El Niño.

- The trade winds become stronger than usual, pushing more warmer waters towards the Indonesian coast, and making the eastern Pacific Ocean colder than normal.

- Impact: La Nina, the opposite of El Nino, typically brings good rainfall during the monsoon season.

Source: TH

Disclosure Framework on Climate-related Financial Risks, 2024

GS3/Environment and Conservation, Economy

In Context

- The Reserve Bank of India (RBI) has released a draft Disclosure Framework on Climate-related Financial Risks, 2024 for banks to follow.

About

- The regulated entities i.e., banks are meant to disclose information about their climate related financial risks and opportunities for the users of financial statements.

- It acknowledges the importance of the environment and its long-term impact on organisations and the economy as a whole.

What are Climate-related Financial Risks?

- The RBI has defined climate-related financial risks as the potential risks that may arise from climate change or from efforts to mitigate climate change, their related impacts and economic and financial consequences.

- It can impact the financial sector through two broad channels i.e., physical risks and transition risks.

- Physical Risks: It refers to the economic costs and financial losses resulting from the increasing frequency and severity of extreme climate change-related weather events.

- Impact on REs: Expected cash flows to the REs from an exposure may be stressed on the occurrence of a local / regional weather event.

- Chronic flooding or landslides may present a risk to the value of the collateral that REs have taken as security against loans.

- Severe weather events may damage a RE’s owned or leased physical property and data centers, thereby, affecting its ability to provide financial services to its customers.

- Transition Risks: It refers to the risks arising from the process of adjustment towards a low-carbon economy.

- A range of factors influences this adjustment, including changes in climate-related policies and regulations, the emergence of newer technologies, shifting sentiments and behaviour of customers.

- The process of transition i.e., reducing carbon emissions may have a significant impact on the economy.

About the Framework:

- All India financial institutions, and top and upper layer NBFCs will have to begin to provide information on governance, strategy, and risk management strategy from 2025-26 and begin disclosure metrics and targets from 2027-28.

- Banks will be mandated to disclose those climate-related risks which have a bearing on their financial stability.

- The revelation will foster an early assessment of climate-related financial risks and opportunities and also facilitate market discipline.

- Organisations under the Purview:

- All scheduled commercial banks (excluding local area banks, payments banks and regional rural banks).

- All Tier -IV primary (urban) and cooperative banks (UCBs).

- All top and upper layer non-banking financial companies.

- Disclosure by the REs:

- Identified climate-related risks and opportunities over short, medium and long term.

- The impact of climate-related risks and opportunities on their businesses, strategy and financial planning.

- The resilience of the RE’s strategy taking into consideration the different climate scenarios.

Significance

- There is an urgent need for a better and consistent disclosure framework for regulated entities, without which the financial risks can lead to mispricing of assets and misallocation of capital.

- This essentially led to a standard disclosure framework on climate related financial risks.

Framework for Regulatory Sandbox

Syllabus: GS3/Economy

Context:

- Recently, the Reserve Bank of India (RBI) updated the ‘Enabling Framework for Regulatory Sandbox’ framework, and extended certain process timelines.

About the Regulatory Sandbox (RS):

- It allows the regulator, the innovators, the financial service providers, and the customers to conduct field tests to collect evidence on the benefits and risks of new financial innovations, while carefully monitoring and containing their risks.

- Regulators may permit certain regulatory relaxations for the limited purpose of the testing.

- Entities that meet the criteria of minimum net worth of ₹25 lakh as per their latest audited balance sheet are eligible to participate in the RS.

Objectives:

- The primary objective of the RS is to foster responsible innovation in financial services, promote efficiency, and bring benefit to consumers.

- It provides a safe and controlled environment for testing new technologies and services, thereby fostering innovation and efficiency in the financial sector.

Components:

- Controlled Environment: A regulatory sandbox usually refers to live testing of new products or services in a controlled/test regulatory environment.

- Regulatory Relaxations: For the limited purpose of the testing, regulators may (or may not) permit certain regulatory relaxations.

- Collaboration: The RS is a collaboration between the regulator, the innovators, the financial service providers, and the end users.

Implementation:

- The RBI revised the timeline for the completion of various stages of a Regulatory Sandbox to nine months from the previous seven.

- The updated framework requires sandbox entities to ensure compliance with provisions of the Digital Personal Data Protection Act, 2023.

Benefits of RS

- Fosters Innovation: The RS allows for live testing of new products or services in a controlled environment.

- If implemented properly, this could usher in innovations in the industry.

- Promotes Efficiency: The RS is designed to foster responsible innovation in financial services, promote efficiency, and bring benefits to consumers.

- Learning by Doing: The RS fosters ‘learning by doing’ on all sides. It provides a structured avenue for the regulator to engage with the ecosystem and to develop innovation-enabling or innovation-responsive regulations.

- Risk Management: The RS allows the regulator, innovators, financial service providers, and customers to conduct field tests to collect evidence on the benefits and risks of new financial innovations, while carefully monitoring and containing their risks.

- Consumer Protection: The RS ensures that Indian consumers continue to receive the best in class financial services.

- It can lead to better outcomes for consumers through an increased range of products and services, reduced costs, and improved access to financial services.

- Regulatory Compliance: The RS provides an environment for innovative technology-led entities for limited-scale testing of a new product or service that may involve some relaxation in a regulatory requirement before a wider-scale launch.

Challenges related to RS

- Flexibility and Time: Innovators may lose some flexibility and time in going through the RS process.

- However, running the RS in a time-bound manner at each stage can mitigate this risk.

- Regulatory Ambiguity: The RS usually refers to live testing of new products or services in a controlled/test regulatory environment for which regulators may (or may not) permit certain regulatory relaxations for the limited purpose of the testing.

- This could lead to regulatory ambiguity.

- Risk Containment: The RS is a controlled mechanism within which the sector will be able to experiment with solutions in a closely-monitored ecosystem so that the risks do not spread outside it, and the reasons for failure can be analysed.

- Data Confidentiality and Customer Protection: Data confidentiality and customer protection are major areas that also need to be addressed.

- Risks for FinTech products may also arise from cross-border legal and regulatory issues5.

- Legal Safeguards: Investors face risks due to lack of legal safeguards.

Conclusion

- Regulatory Sandbox is not without its challenges and risks. These need to be carefully managed to ensure the successful implementation and operation of the RS.

- The proposed FinTech solution should highlight an existing gap in the financial ecosystem and demonstrate how it would address the problem, and bring benefits to consumers or the industry.

Union Cabinet Approved International Big Cat Alliance

Syllabus: GS3/Environment

Context

- The Union Cabinet approved the creation of International Big Cat Alliance (IBCA) to set up a global network for the conservation of tigers and other big cats.

About

- The alliance was conceived as a multi-country, multi-agency coalition of 96 big cat range countries and others to establish a common platform for conservation.

- Objective: Focus of the Alliance is to conserve seven big cats of the world which includes Tiger, Lion, Leopard, Snow Leopard, Puma, Jaguar and Cheetah.

- In India out of the seven big cats only five — tiger, lion, leopard, snow leopard and cheetah — are found.

- The government also approved a one-time budgetary support of ₹150 crore for a period of five years from 2023-24 to 2027-28.

- Governance: IBCA governance consists of an Assembly of Members, Standing Committee and a Secretariat with its Head Quarter in India.

Conservation efforts of India

- Project Tiger: It was launched in 1973 to protect tigers and their habitats by creating protected areas, improving law enforcement, and involving local communities in conservation efforts.

- Project Cheetahs: Cheetahs have been translocated to India from Namibia and South Africa. In 2022, India signed an MoU with Cambodia for tiger reintroduction in Cambodia.

- India is cooperating with neighboring countries through transboundary landscapes such as Terai Arc and Kanchenjunga with Nepal, Transboundary Manas Conservation Area (TraMCA) with Bhutan, and Sundarbans with Bangladesh.

| Seven Big CatsLion (Panthera Leo) IUCN Status: VulnerableRange: It is mainly found in sub-Saharan Africa. Asiatic lions are found in the Gir National Park.Tiger (Panthera Tigris)IUCN Status: EndangeredRange: Bangladesh, Bhutan, Cambodia, China, India, Indonesia, Laos, Malaysia, Myanmar, Nepal, Russia, Thailand and Vietnam.Snow leopard (Panthera Uncia)IUCN Status: VulnerableRange: Mountainous regions of 12 countries – Afghanistan, Bhutan, China, India, Kazakhstan, Kyrgyz Republic, Mongolia, Nepal, Pakistan, Russia, Tajikistan, and Uzbekistan.Jaguar (Panthera Onca)IUCN Status: Near ThreatenedRange: Most of their population exist in the Amazon rainforest and Pantanal in South America. Brazil accounts for half of the wild jaguars in the world.Cheetah (Acinonyx Jubatus)IUCN Status: VulnerableRange: Initially, they were found in Africa, Russia, South Asia, Iran and the Middle East. Currently, the majority live in east and southern Africa apart from a small population in Iran.Puma (Puma Concolor)IUCN Status: Least Concern (LC) Range: Also known as a mountain lion, the puma is found in North, Central and South America.Leopard (Panthera Pardus)IUCN Status: VulnerableRange: Africa, parts of the Middle East, and Asia |

Source: PIB

Development of Agaléga Island

Syllabus: GS2/International Relations

Context

- Prime Minister Modi and his Mauritian counterpart jointly inaugurated an airstrip and the St James Jetty on North Agaléga Island in the Indian Ocean.

India’s vision for its maritime neighborhood

- Strategic Partnership: By participating in the development of Agaléga, India strengthens its strategic partnership with Mauritius. This partnership is rooted in historical, social, and cultural ties, as well as shared interests in maritime security and economic development.

- Seventy per cent of the inhabitants of Mauritius are of Indian origin.

- Maritime Security: Agaléga’s strategic location in the Indian Ocean makes it significant for maritime security. The development of infrastructure such as the airstrip and jetty enhances Mauritius’ capabilities in marine surveillance and security, contributing to regional stability.

- Capacity Building: The joint development of Agaléga underscores India’s commitment to the vision of Security And Growth for All in the Region (SAGAR), and its willingness to assist smaller maritime nations in building capacity and developing capability.

Importance of Agaléga Island

- Geopolitical Location: Agaléga Island is strategically located in the Indian Ocean, making it potentially valuable for countries seeking to establish a presence in the region. Its position could allow for the projection of power and influence over key maritime routes and trade corridors.

- Security Implications: The presence of Agaléga Island offers strategic advantages for maritime security and surveillance in the Indian Ocean. Its development with facilities such as the airstrip and jetty enhances capabilities for monitoring and safeguarding sea lanes, thereby contributing to regional stability.

- Resource Potential: While Agaléga Island itself does not possess significant natural resources, its location in the Indian Ocean could provide access to potential underwater resources such as oil, gas, or minerals.

- Naval and Maritime Infrastructure: The development of infrastructure on Agaléga Island, including the airstrip and jetty, enhances its suitability for naval and maritime operations.

- Diplomatic Relations: India, with historical ties to Mauritius and interests in maintaining stability in the Indian Ocean, may seek to collaborate with Mauritius in developing and utilizing the island’s resources and infrastructure.

Source: IE

Setting up three new semiconductors plants in India

Syllabus: GS3/science and Technology

Context

- The government approved proposals to set up three semiconductor units in Gujarat and Assam with an estimated investment of Rs 1.26 lakh crore.

Proposed semiconductors plants

- A semiconductor fabrication plant will be set up by Tata Electronics and Taiwan’s Powerchip Semiconductor Manufacturing Corp. (PSMC) in Gujarat’s Dholera.

- The Tata Group will also set up a chip assembly plant in Morigaon, Assam at a cost of Rs 27,000 crore.

- CG Power and Japan’s Renesas will also set up a semiconductor plant in Gujarat’s Sanand at an estimated cost of Rs 7,600 crore.

What is a Semiconductor?

- Semiconductors also referred to as ‘chips’ are highly complex products to design and manufacture, providing the essential functionality for electronic devices to process, store and transmit data.

- The chip comprises interconnections of transistors, diodes, capacitors and resistors, layered on a wafer sheet of silicon.

Global Scenario in Chip Manufacturing

- About 70% of the current global manufacturing capacity is confined to South Korea, Taiwan and China, with the US and Japan making up for much of the rest.

- Taiwan and South Korea make up about 80% of the global foundry base for chips.

- Only one company, the Netherlands-based ASML, produces EUV (extreme ultraviolet lithography) devices, without which it is not possible to make an advanced chip.

Challenges

- India’s close allies, like the US and EU, also sense the semiconductor opportunity and have rolled out more lucrative incentive schemes than India.

- Talent pool: While India is the biggest back office for design engineers of all major chip companies, skilled talent that can work on factory floors of a fabrication plant is still hard to come by.

- Research and Development: India currently lacks original research in semiconductor design, where the future of the chip is decided.

- Power supply: Besides, an uninterrupted supply of power is central to the process, with just seconds of fluctuations or spikes causing millions in losses.

- Water intensive: Chip-making also requires gallons of ultrapure water in a single day. This requirement could be a task for the government to provide to factories, compounded also by the drought conditions which often prevail in large parts of the country.

Significance of the project

- Job Creation: The semiconductor industry is highly labor-intensive, requiring skilled engineers and technicians. Semiconductor manufacturing facilities in India will create many direct and indirect employment opportunities.

- Reduced Dependence on Imports: India currently relies on imported semiconductor chips for various electronic devices. Establishing a domestic semiconductor industry will enhance the country’s self-reliance and resilience in times of geopolitical tensions or disruptions in global supply chains.

- Export Opportunities: With a competitive semiconductor industry, India can export chips and related products to other countries, generating revenue and improving its trade balance.

- Strategic Importance: Semiconductor chips are critical components in various strategic sectors such as defense, aerospace, and telecommunications. Having a domestic semiconductor industry ensures greater control over the supply chain and reduces vulnerabilities to disruptions or external pressures.

| India’s Initiatives for Semiconductor IndustryIndia Semiconductor Mission: It has been set up as an Independent Business Division within Digital India Corporation having administrative and financial autonomy to formulate and drive India’s long-term strategies for developing semiconductors and display manufacturing facilities and semiconductor design ecosystem. Production Linked Incentive scheme: Incentives are being provided for semiconductor design and packaging.QUAD Semiconductor Supply Chain Initiatives: To assess the capacity, pinpoint vulnerabilities, and enhance supply chain security for semiconductor and its critical components. |

Way Ahead

- By establishing a semiconductor industry, India can increase its influence in the global technology landscape.

- India can also attract foreign investment, foster innovation, and stimulate other sectors such as electronics, telecommunications, and information technology. A robust industry will significantly contribute to India’s GDP growth.

Source: IE

Syllabus: GS2/Government Policies and Interventions

Context:

- The Union Cooperation Minister launched the National Urban Co-operative Finance and Development Corporation Limited (NUCFDC), the Umbrella organisation for the Urban Cooperative Banks in New Delhi.

- Setting up of the umbrella organization is another milestone in achieving the goal of ‘Sahakar se Samriddhi’ to make ‘Aatma Nirbhar’ Bharat.

National Urban Co-operative Finance and Development Corporation Limited (NUCFDC)

- Established: March 2024

- Aim: To modernize and strengthen the Urban Cooperative Banking Sector in India, ultimately benefiting both the banks and their customers.

- Parent ministry: Ministry of Cooperation, Government of India.

- Objectives:

- Raise capital: NUCFDC plans to reach a capital base of Rs. 300 crores to support Urban Cooperative Banks.

- Provide specialized services: Offer financial assistance, consultancy services, and capacity building programs to UCBs.

- Develop shared technology platform: Besides offering liquidity and capital support, the umbrella organization would set up a technology platform that can be shared by all UCBs, enabling them to widen their range of services at a relatively lower cost.

- It can also offer fund management and other consultancy services.

- Facilitate communication and regulation: Act as a bridge between UCBs and regulatory bodies for better communication and streamlined regulations.

- Current status:

- The NUCFDC has received Certificate of Registration (CoR) from the Reserve Bank of India to operate as a Non Banking Finance Company (NBFC) and serve as the umbrella organization for the urban cooperative banking sector.

- In addition to this, it will be allowed to operate as a Self-Regulatory Organization (SRO) for the sector.

Significance

- Modernization: By being part of NUCFDC, most of these banks would be able to upgrade to the latest technology and will be able to offer new products and services.

- Improved services: By enhancing UCB capabilities, NUCFDC can contribute to improved financial services for urban customers.

- Strengthening cooperative banking: A stronger UCB sector can play a more significant role in India’s financial landscape, offering competitive services and contributing to financial inclusion.

- Grassroot development: This umbrella organization has a potential to bring positive transformation at the grassroots level by empowering the communities across the nation.

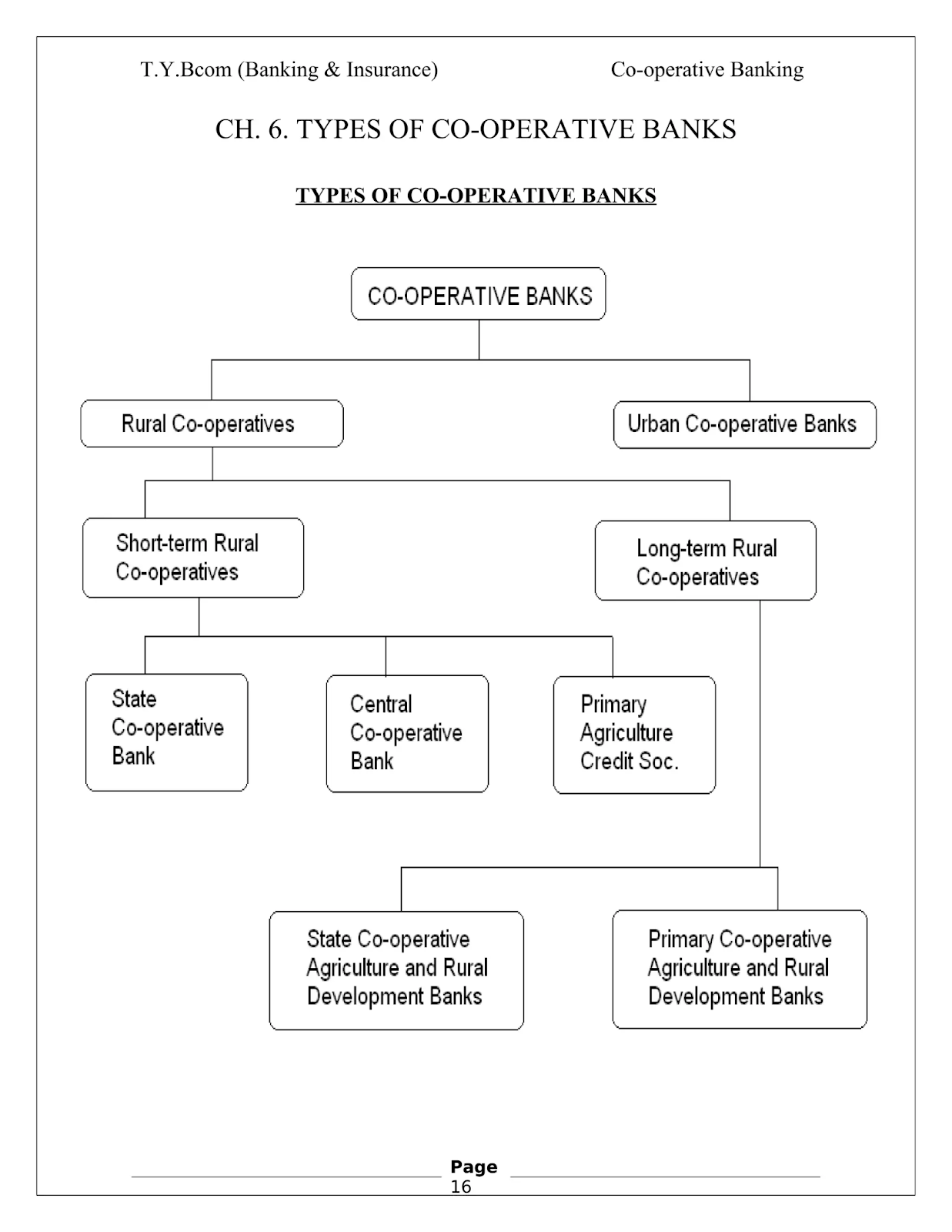

Cooperative Banks in India: An Overview

- Cooperative banks are small financial institutions, which operate both in urban and non-urban centers.

- They play a vital part in India’s financial system by catering primarily to a specific clientele and playing a crucial role in financial inclusion.

- At present, there are over 1,500 scheduled and non-scheduled Urban Cooperative Banks in India with a total number of branches exceeding 11,000.

- The banks have a deposit size of over Rs 5.33 lakh crore, and total lending of more than Rs 3.33 lakh crore.

Regulation and Supervision:

- Dual regulation: There is duality of control over these banks with banking related functions being regulated by the Reserve Bank and management related functions regulated by respective State Governments/Central Government.

- The Reserve Bank of India (RBI) oversees financial aspects like licensing, capital adequacy, and regulations under the Banking Regulations Act 1949.

- State governments, through their Registrar of Cooperative Societies, handle registration, governance, and some administrative aspects.

Types of Cooperative Banks

Significance of Cooperative Banks:

- Financial Inclusion: They play a crucial role in providing financial services to people in rural and underserved areas where commercial banks might not have a presence.

- Supporting Agriculture: They offer credit and other financial services to farmers, contributing to agricultural development.

- Promoting Savings: Cooperative banks encourage savings habits among rural and semi-urban populations.

- Meeting Local Needs: They cater to specific local needs, providing loans for small businesses, housing, and other purposes.

Challenges Faced by Cooperative Banks:

- Limited Capital Base: Smaller capital reserves compared to commercial banks can restrict their lending capacity.

- Governance Issues: Concerns exist regarding governance practices in some cooperative banks.

- Competition: Increased competition from commercial banks and microfinance institutions in some areas.

- Technology Adoption: Lag in adopting modern technologies can hinder efficiency and customer service.

Way Ahead:

- The future of cooperative banks in India depends on their ability to address associated challenges, embrace technological advancements, and adapt to the evolving financial landscape.

- They can continue to play a significant role in financial inclusion and contribute to the economic development of rural and urban communities in India.

Source: PIB

News in Short

PM Surya Ghar Muft Bijli Yojana

Syllabus: GS2/Government Policy and Intervention; GS3/Renewable Energy;

Context:

- Recently, the Union Cabinet approved PM Surya Ghar Muft Bijli Yojana to provide 300 units of free electricity to 1 crore families.

About the PM Surya Ghar Muft Bijli Yojana:

- It aims to light up 1 crore households by providing up to 300 units of free electricity every month, marking a significant step towards sustainable development and people’s wellbeing.

- It was launched with an investment of over Rs. 75,000 crores.

Implementation:

- Under this scheme, households will be provided with a subsidy to install solar panels on their roofs.

- Households can register themselves on the PM Surya Ghar website (https://pmsuryaghar.gov.in) to avail benefits under the scheme.

Financial Assistance:

- The subsidy will cover up to 40% of the cost of the solar panels. The remaining costs have to be borne by the aspirant consumer.

- The Centre will fund 60% of the cost for installing 2 kW (kilowatt) systems and 40% of the cost for systems from 2-3 kW capacity.

- Systems of higher wattage will not be eligible for Central subsidy.

- At current benchmark prices, this will mean ₹30,000 subsidy for 1 kW system, ₹60,000 for 2 kW systems and ₹78,000 for 3 kW systems or higher.

Other Features of the Scheme:

- A Model Solar Village will be developed in each district of the country to act as a role model for adoption of rooftop solar in rural areas.

- Urban Local Bodies and Panchayati Raj Institutions shall also benefit from incentives for promoting RTS installations in their areas.

- The scheme provides a component for payment security for renewable energy service company (RESCO) based models as well as a fund for innovative projects in RTS.

Benefits:

- It includes free electricity for households, reduced electricity costs for the government, increased use of renewable energy, and reduced carbon emissions.

- It is a significant step towards promoting the use of renewable energy in India.

- It is estimated that the scheme will create around 17 lakh direct jobs in manufacturing, logistics, supply chain, sales, installation and other services.

GDP Vs GVA

Syllabus: GS3/ Economy

Context

- According to the Ministry of Statistics and Programme Implementation India’s GDP spiked to a six-quarter high of 8.4% in Q3 FY24, while GVA growth stood at 6.5% during the same period.

Gross Value Added (GVA)?

- GVA quantifies the value of goods and services produced in a country, deducting the cost of inputs and raw materials.

- It adjusts GDP by factoring in subsidies and taxes on products.

How Does GVA Differ From GDP?

- Gross domestic product (GDP) measures the value of all of the total goods and services produced in a country.

- Gross value added (GVA) is the value added to these products to enhance the various aspects of them.

- GVA takes the GDP and adds to the value of subsidies paid on those products and then subtracts out taxes paid on them.

Source: IE

PM-JANMAN

In Context

- The implementation of PM Janjati Adivasi Nyay Maha Abhiyaan (PM-JANMAN) has been slowing down due to simultaneous data collection of beneficiaries under the scheme.

About the PM-JANMAN

- The Union Cabinet approved the scheme in 2023 and the scheme is implemented during FY 2023-24 to 2025-26.

- The Mission would provide PVTG families and communities (Particularly Vulnerable Tribal Groups) essential services.

- The 11 crucial interventions including Central Sector and Centrally Sponsored Schemes through 9 Ministries, including the Ministry of Tribal Affairs include:

- Provision of pucca houses;

- Connecting roads;

- Providing Piped water supply;

- Ensuring Community water supply;

- Providing Mobile medical units with medicine cost;

- Construction of hostels;

- Providing Vocational education and skilling;

- Construction of Anganwadi Centres;

- Construction of Multipurpose Centres (MPC).

| PVTGsIn 1973, the Dhebar Commission set up a separate category for Primitive Tribal Groups (PTGs).PVTGs are a more vulnerable group among tribal groups in India. These groups have primitive traits, geographical isolation, low literacy, zero to negative population growth rate and backwardness. Moreover, they are largely dependent upon hunting for food and a pre-agriculture level of technology.Population: The 2011 census of India had put the Vulnerable Tribal Population at 10.45 Crore in 75 communities spread across 18 States and the Union Territory of Andaman and Nicobar Islands,Odisha has the largest population of PVTGs followed by Madhya Pradesh. |